Seniors: About Medicare Advantage Plans

A comprehensive clinical guide to Medicare Part C, detailing networks, supplemental benefits, and out-of-pocket maximums specifically designed for seniors.

Understanding Medicare Advantage: Essential Information for Seniors

Medicare Advantage, also known as Medicare Part C, has grown to become one of the most preferred options for older adults seeking Medicare coverage. However, the variety of rules, network restrictions, and associated costs can often be overwhelming—especially when trying to compare different plans during the open enrollment period.

Figure 1: Medicare Advantage plans are provided by private insurance companies as an alternative to Original Medicare.

This article simplifies everything using clear, senior-friendly language, concentrating on topics such as “Medicare managed care,” “Part C supplemental benefits,” and the crucial “Medicare Advantage out-of-pocket maximum.”

What Exactly Is Medicare Advantage (Part C)?

Medicare Advantage is a comprehensive alternative to Original Medicare, combining multiple coverages into one plan. These plans are offered by private insurers approved by Medicare and must comply with federal regulations.

Typically included in most plans:

- Part A (Hospital insurance)

- Part B (Medical insurance)

- Part D (Prescription drug coverage)

- Additional Benefits: Coverage often extends to dental, vision, hearing, fitness programs like SilverSneakers, transportation services, and allowances for over-the-counter (OTC) items.

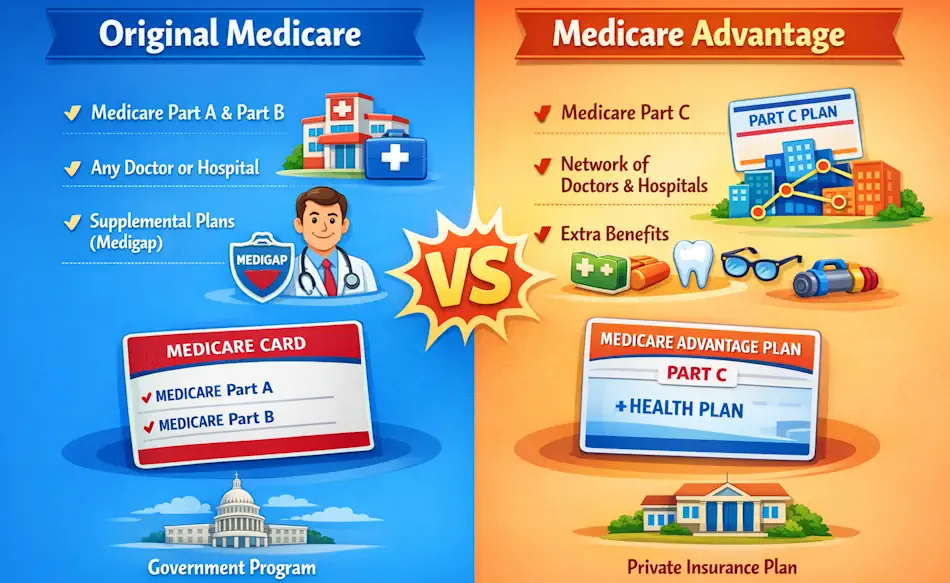

Figure 1: Side‑by‑side comparison of Original Medicare and Medicare Advantage, highlighting how coverage is structured, provider access, and added benefits to help beneficiaries choose the plan that best fits their health needs.

Figure 1: Side‑by‑side comparison of Original Medicare and Medicare Advantage, highlighting how coverage is structured, provider access, and added benefits to help beneficiaries choose the plan that best fits their health needs.

How Does Medicare Advantage Operate?

Medicare pays private insurance companies to administer your healthcare coverage. In exchange, these plans offer a coordinated care model that aims to manage your health comprehensively.

Important aspects include:

- Network Limitations: Most Medicare Advantage plans require you to use a designated network of doctors and hospitals.

- Out-of-Pocket Maximum: Each plan sets an annual cap on your personal healthcare expenses, which Original Medicare does not provide.

- Care Coordination: A dedicated team monitors your health conditions and appointments to ensure effective communication between your primary care provider and specialists.

Real-World Examples

Case Study #1: Sarah, 72 - “I Needed Dental and Vision Coverage”

Sarah initially had Original Medicare but found dental expenses burdensome. She switched to a Medicare Advantage PPO plan that offered two dental cleanings annually, new glasses each year, and a $50 monthly OTC card. This change lowered her out-of-pocket costs and simplified her care with a single insurance card.

Case Study #2: John, 68 - “My Medications Were Too Costly”

John, who manages diabetes, faced high medication costs under Original Medicare. He opted for a Medicare Advantage plan with no premium and a low-cost insulin program, which significantly reduced his yearly medication expenses.

Advantages and Important Considerations

Benefits:

- Comprehensive Coverage: Combines hospital, medical, and prescription drug coverage into one plan.

- Cost Predictability: The out-of-pocket maximum safeguards your finances against extreme medical expenses.

- Coordinated Care: Access to nurse advice lines and chronic disease management programs.

Things to Watch For:

- Network Constraints: HMOs generally require you to stay within the network, while PPOs offer more flexibility but may cost more.

- Prior Authorization: Some treatments or services need approval from the plan before coverage is granted.

- Drug Formularies: It’s essential to review the plan’s list of covered medications to ensure your prescriptions are included at affordable tiers.

Frequently Asked Questions About Medicare Advantage Plans

1. How does Medicare Advantage differ from Original Medicare?

Medicare Advantage combines Parts A, B, and often D into a single plan with additional benefits. Original Medicare includes only Parts A and B, often requiring a separate Part D plan and a Medigap policy for extra coverage.

2. Can I keep my current doctor?

Yes, as long as your doctor participates in the plan’s network. Always confirm network participation before enrolling.

3. Are Medicare Advantage plans more affordable?

Many plans have $0 premiums, but you still must pay your Part B premium. Overall costs depend on your specific copayments and deductibles.

4. Is it possible to return to Original Medicare?

Yes, you can switch back during the Annual Enrollment Period (October 15 to December 7) or the Medicare Advantage Open Enrollment Period (January 1 to March 31).

Glossary of Medicare Terms for Aging Health

Medicare Advantage (Part C)

A private insurance option that combines hospital, medical, and prescription drug coverage into a single plan, often with extra benefits.

Formulary

The list of prescription medications covered by a plan, organized into different cost tiers.

Out-of-Pocket Maximum

The highest amount you will pay in a year for covered healthcare services, providing essential protection against large medical bills.

About the Author

Tommy T. Douglas is an independent health researcher and patient advocate. Having survived a major heart attack in 2008 and managing Type 2 Diabetes, he focuses on translating complex medical information into practical health guidance tailored for seniors.

| Discover more articles: Heart | Metabolism | Brain | Liver |

Clinical Sources and References

- Centers for Medicare & Medicaid Services – Overview of Medicare Advantage

- National Council on Aging – Guide to Medicare Options

- Kaiser Family Foundation – Trends in Medicare Advantage