Navigating Medicare in 2026: A Senior’s Guide to Coverage & Advocacy

A comprehensive 2026 guide to Medicare, covering the new $2,000 drug cap, enrollment strategies, and choosing between Original Medicare and Advantage.

Why Medicare Literacy is Part of Your Health Defense

For a senior managing chronic conditions—whether it’s Type 2 Diabetes, heart health, or vascular resilience—Medicare is more than just insurance; it is the financial engine of your healthcare. In 2026, the system has seen its most significant reforms in decades. Understanding these changes ensures you don’t just have coverage, but that you have access to the specific clinical protocols that maintain your healthspan.

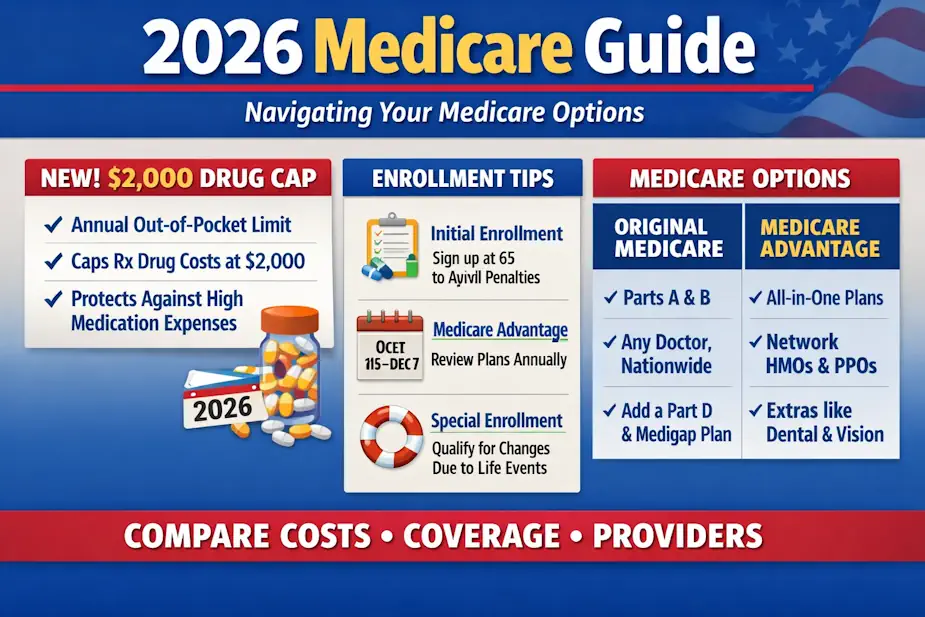

Figure 1 Your 2026 Medicare roadmap—understand the new $2,000 drug cap, smart enrollment timing, and how to choose between Original Medicare and Advantage for better coverage and savings.

Figure 1 Your 2026 Medicare roadmap—understand the new $2,000 drug cap, smart enrollment timing, and how to choose between Original Medicare and Advantage for better coverage and savings.

2026 Milestone: As of January 1, 2026, the out-of-pocket spending cap for prescription drugs (Part D) is strictly limited to $2,000 per year. This is a game-changer for those on high-cost medications like GLP-1s or advanced cardiovascular therapies.

The Four Pillars of Medicare (2026 Edition)

Part A: Hospital Insurance

- What it covers: Inpatient hospital stays, skilled nursing facility care, hospice, and some home health care.

- The 2026 Cost: For most who paid Medicare taxes, the premium is $0. However, the deductible for each “benefit period” has adjusted for inflation (approx. $1,700 in 2026).

Part B: Medical Insurance

- What it covers: Doctor visits, outpatient care, medical supplies, and preventive services (like your annual wellness exams and screenings).

- Advocacy Tip: Part B covers the “Vascular Bridge” diagnostics we discuss, such as hs-CRP and RCDW testing, if deemed medically necessary for managing existing conditions.

Part C: Medicare Advantage

- What it is: An “all-in-one” alternative to Original Medicare, offered by private companies.

- The Trade-off: Often includes “extras” like vision or dental, but uses restricted provider networks. In 2026, ensure your specific specialists are in-network, as many plans have narrowed their lists.

Part D: Prescription Drug Coverage

- The Big Change: In addition to the $2,000 cap, you now have the option to use the Medicare Prescription Payment Plan (M3P), which allows you to spread your drug costs into monthly installments throughout the year rather than paying a large chunk at the pharmacy counter.

Choosing Your Path: A Decision Tool

| Feature | Original Medicare + Medigap | Medicare Advantage (Part C) |

|---|---|---|

| Doctor Choice | Any doctor in the US who accepts Medicare. | Usually restricted to a local network. |

| Costs | Higher monthly premium; very low per-visit cost. | Low/Zero monthly premium; copays for every visit. |

| Referrals | No referrals needed for specialists. | Usually requires a PCP “gatekeeper.” |

| Drug Coverage | Requires a separate Part D plan. | Usually included in the plan. |

📅 Enrollment Guardrails

Missing your window can lead to lifetime penalties. Protect your healthspan by tracking these dates:

- Initial Enrollment Period (IEP): The 7-month window around your 65th birthday.

- General Enrollment Period (GEP): January 1 – March 31 annually (coverage starts the following month).

- Annual Enrollment Period (AEP): October 15 – December 7. This is when you should review your Part D plan to ensure your 2026 drug costs stay under that $2,000 cap.

Real-Life Case Studies

Case 1: The Diabetic Advocate (Managing Type 2)

“John” uses a CGM (Continuous Glucose Monitor) and Ozempic. In 2025, his drug costs were nearly $4,500. Under the 2026 Part D Cap, his costs dropped to exactly $2,000, and he opted for the M3P payment plan to pay roughly $166/month, stabilizing his household budget.

Case 2: The Heart Attack Survivor (Original Medicare)

“Sarah” has a history of vascular risk and prefers her out-of-state cardiologist. She chose Original Medicare + Medigap Plan G. While her monthly premium is higher, she has zero copays for her regular “Vascular Bridge” blood work and no “gatekeeper” delays for her stress tests.

🔬 Medicare Glossary (2026)

| Term | Definition |

|---|---|

| Doughnut Hole | EXTINCT. As of 2025/2026, the “coverage gap” is gone. You move straight from your deductible to the $2,000 cap. |

| M3P | Medicare Prescription Payment Plan; the new “smoothing” option for drug costs. |

| Extra Help | A federal program for low-income seniors that has been expanded in 2026 to cover more people. |

| Creditable Coverage | Insurance (like from a former employer) that is at least as good as Medicare Part D. |

❓ Frequently Asked Questions

Q: Does Medicare cover the “Biological Age” tests mentioned on this site? A: Standard labs (like Albumin or Creatinine) are covered. Specialized tests like hs-CRP are covered if you have a documented risk of heart disease or inflammatory conditions. Use our Doctor’s Script to help your physician code these correctly.

Q: What happens if I spend more than $2,000 on drugs? A: Once you hit $2,000 in out-of-pocket costs for covered Part D drugs, your plan pays 100% of your drug costs for the rest of the year.

Q: Can I switch from Advantage back to Original Medicare? A: Yes, during the AEP or the Medicare Advantage Open Enrollment Period (Jan 1 – Mar 31). However, be aware that getting a Medigap policy later in life may require “medical underwriting” depending on your state.

Conclusion: Be Your Own Best Advocate

Medicare in 2026 is more supportive than ever, but it requires active management. Don’t let your coverage happen to you. Review your “Evidence of Coverage” (EOC) annually and use the $2,000 cap to your advantage to stay consistent with your clinical protocols.

Sources & Further Reading

- Medicare.gov (2026): Official Guide to the Medicare Prescription Payment Plan.

- CMS.gov (2025): Inflation Reduction Act Impact Report for Seniors.

- Aging Health Research (2026): Patient Tools & Lab Trackers.